Financial Teardown #2: Adobe

Translating the Adobe P&L into a POV business narrative sellers can use

If you’re new to this series, check the the framework you can use to synthesize and message based on what you learn from a company’s financials.

Like last week, the core question doesn’t change:

How would a CFO look at this?

This week we’re covering Adobe and breaking down how you’d sell into their world if you were in the shoes of a seller at Pigment.

The structure:

Read the business engine → translate the financial reality → strategic priority → build the narrative

Let’s dive in.

Financial Teardown # 2: Adobe

For consistency, I’m referencing Adobe’s 2024 10-K (their fiscal ends on the Friday closest to November 30th).

If I were prospecting today, I’d pull their Q3 10-Q and earnings calls to get the most up to date signals. If Adobe was an active deal, I’d be on the lookout for their 2025 10-K due to release December 10th .

What we’ll cover today

The business engine

How the business makes money

The financial signal

The strategy that matters to leaders

The sales translation

NOTE: If you have an account you’d like me to teardown, DM or email andrew@hackingsales.xyz. Subscribers are prioritized and details are kept anonymous.

The Business Engine

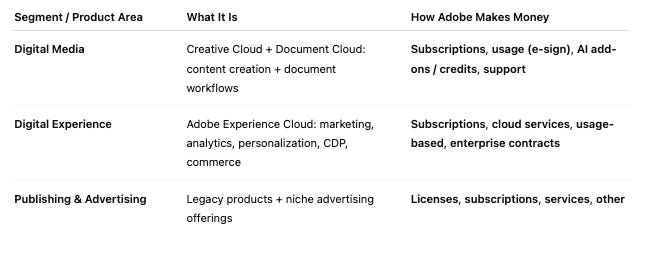

Adobe is broken out into 3 segments:

NOTE: This is a mental model for how I’d go about account planning. These are hypotheses I’m drawing off public data. You need to validate with prospects.

Do your due diligence with internal data. Reference your CRM, Gong, etc. to further refine and understand how your prospects are talking about projects, orgs, initiatives, etc.

Takeaways:

P&L is clearly distributed across each segment. Unlike Salesforce, segments do not ladder up into a unified mission.

Salesforce clouds are “mini businesses” that serve one buyer journey.

Adobe’s segments serve different customers, different workflows, and different different economics.

Their P&L’s aren’t separate versions of one business - they’re separate businesses.

Adobe is predominantly an “ARR” machine, accompanied by smaller revenue streams (ie, licensing, advertising, and services). They exist not to maximize margin but to support workflows, increase stickiness, and extend customer lifetime value “LTV”.

How Does the Business Make Money?

Adobe isn’t a “creative suite”. Adobe provides customers with an end to end content pipeline. They own the full lifecycle: creation → activation → management → measurement.

Each segment monetizes a different part of the content engine:

Digital Media

Creative Cloud: “Create more.” Tools for producing assets, videos, and designs.

Document Cloud: “Work smarter.” PDF, e-sign, and document automation.

Digital Experience

Experience Cloud: “Activate and measure.” Marketing, analytics, personalization, and commerce.

Publishing & Advertising

Legacy Products: “Support and extend.” OEM, PDF licensing, and ad-tech.

Adobe’s ecosystem isn’t horizontal like Salesforce - it’s vertical. Unified around a single workflow: the content pipeline.

Salesforce sells to one department, many workflows.

Adobe sells to multiple departments, one workflow.

AI is deeply embedded across all segments, which matters heavily in their financials and leadership focus. More on that below.

The Financial Signal

Topline

Digital Media subscription revenue expansion

Experience Cloud contract growth

RPO expansion

Takeaway: Subscription growth is predictable, but leadership needs AI monetization to accelerate ARR without inflating CAC (customer acquisition cost).

Profitability

High gross margins in Digital Media

Balance mixed margins in Digital Experience (enterprise services + infra costs)

Operating income expansion

Takeaway: AI investments must convert into margin-accretive revenue growth and protect Digital Media, it’s highest margin business.

NOTE: EPS (earnings per share) expansion is a key investor focus, but as sellers, focus on the metrics that drive EPS, not EPS itself.

Efficiency

OPEX discipline

GTM Productivity

R&D Leverage

Takeaway: operational leverage is essential - this is how Adobe funds the AI roadmap. Each incremental ARR dollar is fuel for AI.

Cash Flow

Robust free cash flow

Strong deferred revenue

Predictable cash generation

Takeaway: cash needs to be measured and produce disproportionately higher ARR. Strong cashflow means aggressive AI investment without sacrificing financial stability.

NOTE: Patterns emerge across companies and categories. Like Salesforce, Adobe isn’t increasing spend to fund AI - they’re increasing efficiency to fund it.

The Strategy that Matters to Leaders

What the CFO Cares Most About

Make AI a durable revenue engine, not hype

Prove AI is accretive to ARR and margins.

De-risk AI: compliance, IP, customer trust

Takeaway: AI must be measured like an economic engine - every dollar tied to ARR, margin, and cash flow impact.

What the Company Is Focused On

Three-Cloud AI integration

Firefly → creative workflows

Acrobat AI → document workflows

Agentic AI → enterprise workflows

AI-influenced ARR as KPI (>$5B, explicit goal to double)

Agentic AI workflows for automating cross-cloud processes

Enterprise expansion and deeper account wallet share

Strategic Initiative: Turn AI from a feature into a measurable financial engine.

What’s Getting in Their Way

Competitive pressure in AI (Canva, Figma, AI startups)

Investor skepticism on long term pricing power

Perception risk around training data and creative IP

Portfolio complexity across clouds and SKUs

Strategic Initiative: Move fast in AI and prove the economics. Defend pricing power. Simplify the value story.

NOTE: Adobe’s value story isn’t an easy task. If the CFO struggles to articulate, imagine selling.

I included investor-related signals in this breakdown: they correlate and sometimes directly shape the pressure prospects feel inside accounts. And oh yea, remember the Figma acquisition deal?

The Sales Translation

Pigment:

If I were selling Pigment, I’m not pitching “FP&A” software.

I’m helping Adobe built a financial intelligence layer that connects AI adoption, subscription economics, and segment performance into unified model leadership can use to steer the business.

Value Pillars:

unify financial + operational signals (ARR, usage, AI credits, retention, infra cost)

run real-time “what-if” scenarios on AI adoption, pricing, and product mix

shorten planning cycles so AI performance flows into guidance sooner

give CFO + BU leaders a shared, trusted source of truth for AI economics

make AI’s impact on ARR, margins, cash flow, and EPS clearly measurable

Example narrative:

Finance teams at SaaS companies are under pressure to prove that AI investments translate into measurable financial returns - ARR growth, margin expansion, and stronger free cash flow.

Pigment gives FP&A teams the clarity and real-time modeling to tell that story: showing exactly how AI impacts the P&L, improving forecast accuracy, and enabling decisions that strengthen long-term performance.

Hope this was helpful.

If you have an account you’d like me to teardown, DM or email andrew@hackingsales.xyz. Subscribers are prioritized and details are kept anonymous.

Any other questions, comments, thoughts? Send them my way, contact info above.

As always, thanks for reading and see you all next week.

-Andrew K

PS - if you liked this article, feel free to give a “like”, “comment”, or “share” with your network

Couldn't agree more. How do segments inform financial strategy?

The point about AI needing to be an economic engine rather than just a feature is spot on. A lot of companies are treating AI adoption as a binary metric when the real question is whether each AI dollar generates more margin and ARR than the alternative. Adobe's challenge with proving that equation is probably why they're so aggressive on the enterprise wallet share play right now.